📊 Energy & Monetary Policy | June 2026

OPEC Pumps.

RBI Pulls.

India Balances.

Two big decisions happened at almost the same time — one in Vienna, one in Mumbai. OPEC+ voted to increase oil output significantly, flooding global markets with more crude. And the RBI, watching a softening economy, started rolling out measures to attract more foreign money into India.

On the surface, these look like two separate stories. But for India — the world’s third-largest oil importer — they’re deeply connected. More oil supply could mean lower import costs. More foreign inflows could stabilise the rupee. Together, they could either give India a real economic tailwind — or cancel each other out in ways that professionals need to understand.

This isn’t a simple good-news story. There are real trade-offs, real transmission risks, and real implications for where Indian markets, monetary policy, and corporate earnings go from here.

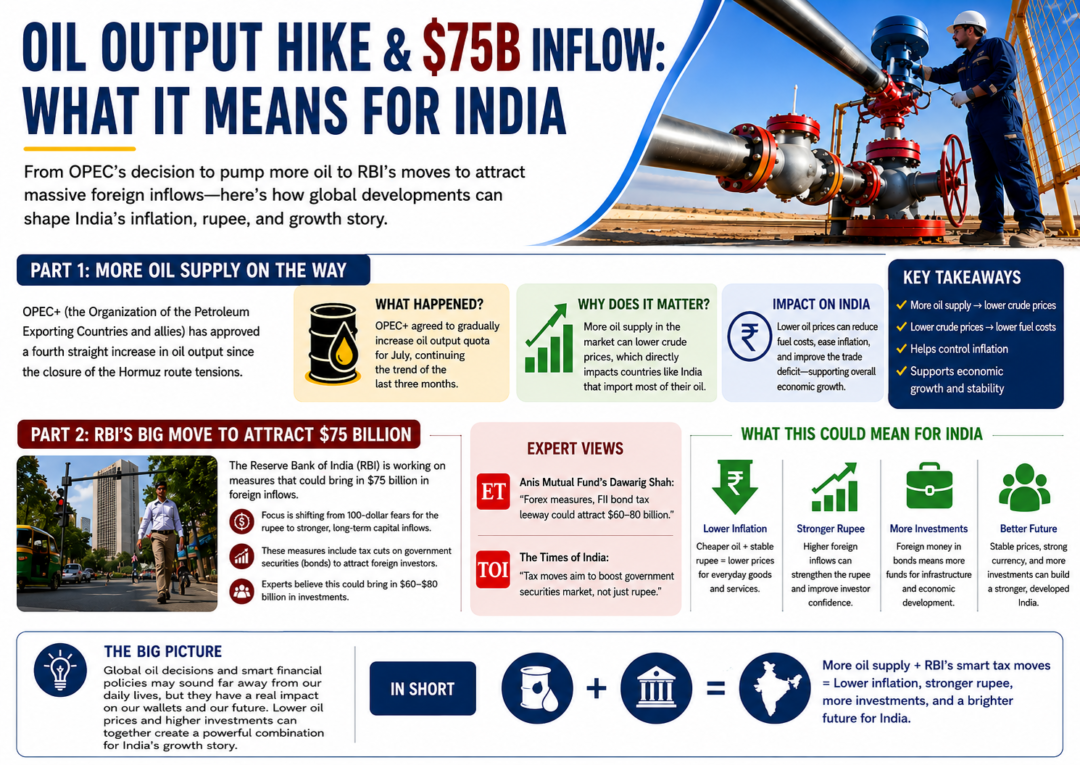

What OPEC+ Actually Did — And Why It Matters

In May 2026, OPEC+ announced a production increase of around 411,000 barrels per day — continuing a gradual unwind of the cuts it had been holding since 2022. The decision wasn’t a surprise to seasoned watchers, but the pace of the rollback was faster than consensus expected.

The stated reason was straightforward: global demand remains solid, and member countries — led by Saudi Arabia and the UAE — want to regain market share before non-OPEC supply (especially U.S. shale) grows into the gap. There’s also a fiscal dimension. Gulf sovereigns need oil above certain thresholds to fund their domestic budgets and Vision-style economic transformation programs.

The India Transmission Mechanism

Here’s the direct line from OPEC’s production decision to India’s economy. India imports roughly 85% of its crude oil requirements. Every $10 drop in Brent crude reduces India’s annual import bill by approximately $12–15 billion. That’s not a rounding error — it’s a meaningful improvement in the current account deficit.

Lower import costs also ease pressure on the rupee. When oil is expensive, more dollars flow out to pay for it, weakening the currency. When oil softens, that outflow shrinks. It’s one of the most direct and cleanest transmission mechanisms in India’s macroeconomic toolkit — and it doesn’t require any policy action to kick in.

RBI’s Foreign Inflow Play — Reading Between the Lines

At the same time OPEC was loosening the oil tap, the RBI was working on a different problem: keeping dollars coming into India. The central bank has been rolling out a package of measures designed to make India more attractive for foreign capital — both debt and equity flows.

The moves include relaxing limits on foreign portfolio investment in government bonds, offering more flexible hedging instruments to overseas investors, and signalling a longer rate-softening cycle. The RBI has already cut rates by 50 basis points in 2026, with more potentially on the table.

🔑 What RBI’s Inflow Measures Actually Cover

- Fully Accessible Route (FAR) Bonds: Expanding the pool of government securities accessible without FPI limits. This directly targets global bond index inclusion flows — a potential $25–30 billion opportunity as India deepens its presence in JPMorgan and Bloomberg bond indices.

- NRI Deposit Incentives: Higher interest rate ceilings on FCNR(B) deposits to attract non-resident Indian savings. When global rates are volatile, competitive NRI rates become a meaningful tool for rupee stabilisation.

- Flexible Hedging Framework: New OTC derivatives framework making it cheaper and easier for foreign investors to hedge rupee exposure. This lowers the effective cost of holding Indian assets for overseas institutions.

- Rate Softening Signal: With CPI trending down and growth concerns rising, the RBI has signalled a continued accommodative tilt — making Indian duration assets relatively more attractive compared to peers where rate cuts are less certain.

The strategic intent here is clear. India wants to be a destination for foreign capital — not just FDI in manufacturing, but portfolio flows that deepen the bond and equity markets, provide rupee support, and fund the current account. The RBI is essentially building a financial infrastructure to absorb that capital safely.

“India doesn’t just need cheap oil. It needs steady dollars. The RBI is making sure both channels stay open at the same time.”

Macro Strategy Desk — June 2026 Perspective

How the Two Forces Interact for India

This is where it gets interesting for professionals. OPEC’s output hike and RBI’s inflow measures aren’t just two parallel stories — they interact in ways that could either amplify each other’s benefits or partially offset them.

Softer oil means less dollar outflow on the import side. Foreign inflows from RBI measures add dollar supply on the capital account side. Both work in the same direction — rupee support. If both channels deliver simultaneously, ₹83–84 could hold with less RBI intervention than the market expects.

Lower crude softens fuel and transport costs, which feeds into WPI and eventually CPI. But India’s food inflation is weather-driven, not oil-driven. So the full disinflationary benefit of cheap oil gets diluted by domestic agricultural factors. The RBI knows this — which is why rate cuts have been measured, not aggressive.

Indian oil marketing companies (IOCL, BPCL, HPCL) benefit from lower crude through improved refining margins and reduced under-recoveries. When crude softens and retail prices don’t fall proportionally, OMCs book the spread. This is a very direct earnings tailwind — and it’s already showing up in quarterly numbers.

India’s inclusion in global bond indices combined with RBI’s lower rate trajectory creates a rare moment: falling yields meeting rising foreign demand. FPI flows into Indian government securities have been accelerating. This compresses borrowing costs for the government — and ultimately for the corporate sector too.

India’s current account deficit is heavily influenced by oil prices. A $10/barrel decline in sustained crude prices can narrow the CAD by roughly 0.3–0.4% of GDP. Combined with services export strength (IT, remittances), the CAD could narrow meaningfully in FY27 — reducing India’s vulnerability to external shocks.

Foreign inflows are not permanent. If global risk appetite shifts — a U.S. recession signal, a Fed pivot reversal, or a geopolitical escalation — FPI money can exit India quickly. The RBI’s frameworks help attract capital but cannot prevent sudden outflows. This remains the key vulnerability in the optimistic scenario.

What Professionals Should Be Doing Now

The macro setup — softer oil plus accommodative RBI plus improving current account — is constructive for Indian assets. But constructive doesn’t mean uncomplicated. Here’s the specific, actionable read for different professional contexts.

For Equity Investors

- OMC re-rating is real: IOCL, BPCL, and HPCL have been chronically undervalued due to refining margin uncertainty. The current environment — lower crude, stable retail prices — creates a window where margin visibility improves. These aren’t exciting businesses, but the re-rating logic is clean.

- Aviation earnings recovery: IndiGo and Air India both carry significant jet fuel cost exposure. A sustained $70–80 Brent environment meaningfully improves unit economics. Watch forward capacity additions — airlines tend to expand aggressively when fuel is cheap, which is both good and a margin risk at the same time.

- Paints and chemicals — indirect beneficiary: Crude derivatives feed into raw material costs for Asian Paints, Berger, and speciality chemical companies. Softer crude means input cost tailwinds without needing to cut prices. Margin expansion is the story here, not revenue growth.

- Banks — bond portfolio relief: Lower yields on government securities improve the mark-to-market position of bank treasury books. PSU banks with large HTM bond portfolios see balance sheet improvement. This is often overlooked in bank analysis but matters for net worth and capital ratios.

For Fixed Income Professionals

- India duration is the play: The combination of falling CPI, RBI rate cuts, and increasing FPI demand for Indian bonds creates a compelling case for longer-duration government securities. The 10-year G-sec yield has room to compress further if macro stays supportive.

- Credit spreads — stay selective: Lower rates don’t automatically tighten all credit spreads. In a global risk-off scenario, India’s lower-rated corporate bonds can widen sharply despite benign domestic macro. Quality over yield-chasing remains the right framework.

- FCNR(B) deposits as a signal: Watch NRI deposit flows as a leading indicator of overseas confidence in the rupee. Strong FCNR(B) inflows signal that the diaspora community — typically well-informed about India-specific risks — is comfortable. A sudden slowdown would be a warning sign.

For Treasury and Corporate Finance Teams

- Hedge oil exposure asymmetrically: With Brent volatile in a wide range, companies with crude exposure should consider options-based hedging rather than fixed forwards. Buying protection against a spike above $90 while participating in the $70–80 downside makes more sense than locking in at current levels.

- External borrowing window: The RBI’s improved hedging framework and compressed domestic spreads make this a reasonable window to evaluate external commercial borrowings (ECBs) for companies with dollar revenue. Hedging costs have come down, and global rates have plateaued.

Three Scenarios Worth Stress-Testing

- Goldilocks (Base Case ~45%): Oil stays $70–80, RBI inflow measures attract steady FPI, rupee trades ₹83–85, CPI holds below 4%, RBI delivers one more rate cut by year-end. Indian equities grind higher, bond yields compress, CAD narrows to 1.2–1.5% of GDP. This is the scenario market consensus is increasingly pricing in.

- External Shock (~30%): Geopolitical escalation in West Asia reverses OPEC output increase. Oil spikes back above $90. Simultaneously, global risk-off triggers FPI outflows from India. Rupee weakens sharply toward ₹87–88. RBI pauses rate cuts. OMC and aviation stocks reverse hard. This is the scenario that gets underweighted until it happens.

- India Outperformance (~25%): OPEC keeps pumping, oil falls toward $65. India’s CAD surplus scenario becomes plausible for the first time in a decade. Bond index flows accelerate, rupee strengthens. RBI cuts rates aggressively, growth surprises on the upside at 7%+. A scenario very few are positioned for — which is exactly why it carries the highest asymmetric return potential if it plays out.

Final Read:

India Is Holding a Rare Hand.

India’s energy import bill is getting cheaper. Its domestic monetary policy is supportive. Its capital account is opening up in structured ways. And its domestic consumption story — the one thing nobody can take away — remains structurally intact.

The risks are real: a West Asia escalation that reverses the oil trend, a global risk-off that pulls FPI money out faster than the RBI’s frameworks can absorb, or domestic political noise that dents institutional credibility. These aren’t hypotheticals — they’re the tail scenarios every serious portfolio manager should be hedging.

But the base case — for maybe the first time in several years — genuinely favours India. The professionals who map this early, position across sectors with real earnings leverage, and hold through the inevitable volatility are the ones who’ll look smart when FY27 numbers land.

Macro Analysis — June 2026