🏦 Banking & Governance | May 2026

HDFC Bank’s

₹45-Crore

Shadow

Deal.

India’s largest private bank doesn’t need to risk its reputation over a few crores. HDFC Bank holds deposits worth nearly ₹31 lakh crore. So when a ₹45-crore payment surfaces — allegedly disguised as marketing spend to funnel higher interest returns to a Maharashtra government agency — the question isn’t really about the money.

The real question is: what does it tell us about how decisions get made at the top of one of India’s most trusted financial institutions?

The MSRDC controversy has landed at a moment when HDFC Bank is already navigating choppy waters — absorbing a massive merger, managing profitability pressures, and now dealing with a boardroom exit that shook investor confidence. This isn’t just a compliance story. It’s a corporate governance story. And those tend to cut a lot deeper.

What Actually Happened Here

Let’s start with the basics — because the way this story is being told matters as much as the story itself.

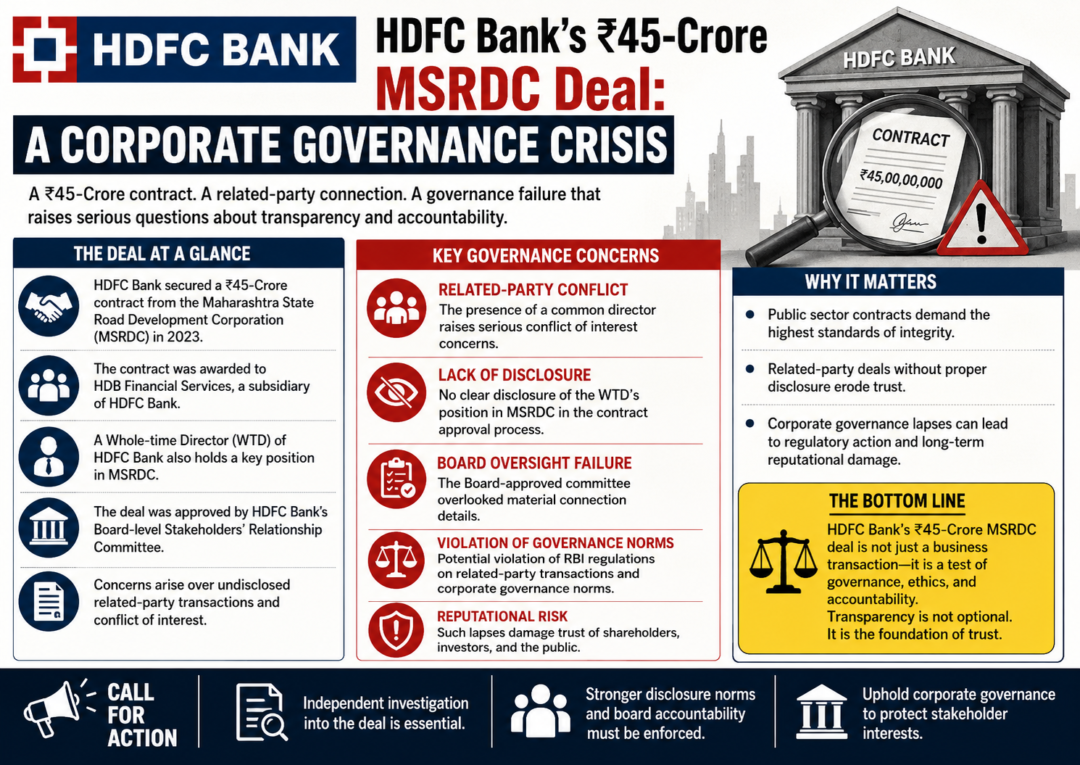

According to an investigation by The Indian Express, HDFC Bank allegedly paid ₹45 crore to the Maharashtra State Road Development Corporation during FY2024 and FY2025. On paper, these were “contributions to a road safety awareness campaign.” In reality, the internal probe reportedly found they were structured to compensate MSRDC for parking large deposits with the bank at a preferential rate — well above what any regular customer would get.

The internal vigilance probe — ordered by the Audit Committee of the Board on March 12, 2026 — reportedly concluded that over ten senior officials carried responsibility for the arrangement. And critically, the probe found that MD & CEO Sashidhar Jagdishan and CFO Srinivasan Vaidyanathan were reportedly present at discussions where this arrangement was devised.

HDFC Bank has maintained that legal firms appointed to review governance claims have yet to find material lapses. But the damage was already visible — the stock fell about 2.5% the day the story broke.

Why the “Marketing Department” Route Is Significant

Routing payments through marketing budgets rather than interest line-items isn’t just an accounting trick. It’s a deliberate structuring decision that sidesteps regulatory reporting. Banks are required to follow RBI-mandated deposit rate guidelines. Interest payments above prescribed limits to specific customers — especially institutional clients — would need to be disclosed and justified.

By labelling the payments as “sponsorship” for road safety campaigns, the arrangement kept those transfers off the radar of standard compliance checks. That’s not a junior employee’s creative accounting. That requires coordination across departments — and, if the probe’s findings are accurate, awareness at the most senior levels.

The Timeline That Nobody Can Ignore

Taken individually, each event in the last few months might look like a coincidence. Together, they paint a more troubling picture.

Six days between the probe order and the chairman’s resignation. That’s the detail that gives this timeline its weight. Whether the two events are directly connected is formally unconfirmed — but the sequence is hard to dismiss.

The Governance Question Nobody Wants to Ask

Corporate governance failures at large Indian banks are rarely dramatic at first. They tend to be quiet — decisions taken in small rooms, language chosen carefully, paper trails structured to pass surface-level scrutiny. That’s what makes them so hard to catch until someone breaks ranks, or an audit flags something unexpected.

What makes this case different is the nature of the alleged arrangement itself. This wasn’t a rogue trader. It wasn’t a single department going off-script. If the probe’s findings are accurate, it involved the marketing department, the CMO, senior leadership, and the CFO’s awareness — all to secure deposits from a government agency that represents a small fraction of HDFC Bank’s total deposit base.

“When the CMO is on record saying his department camouflaged interest payments as marketing spend, that’s not a governance grey area. That’s a structural failure.”

Corporate Governance Desk — May 2026

What the Probe Reveals About Internal Controls

The most unsettling part of this story isn’t that it happened — banks have had compliance failures before. It’s that it apparently took an internal marketing audit to catch it. Not an external regulator. Not a whistleblower alert to the RBI. An internal routine audit that happened to notice the marketing department’s rating was “unsatisfactory.”

That raises legitimate questions about the robustness of HDFC Bank’s internal control architecture. If a ₹45-crore structured arrangement across two financial years — involving disguised interest payments to a state government agency — can pass through undetected until a department audit, what else might be sitting in other departments?

🔑 What Good Corporate Governance Should Have Caught

- Board-level visibility on unusual deposit deals: Any arrangement offering institutional depositors rates materially above market should trigger a board-level review — not a marketing department workaround.

- CFO sign-off transparency: Finance leadership being present at the discussion doesn’t automatically mean approval. But it does mean there was knowledge — and arguably an obligation to flag the arrangement for compliance review.

- Audit Committee independence: To the Audit Committee’s credit, once the marketing audit flagged the issue, they moved quickly — ordering the probe six days before the chairman’s resignation. That’s a positive signal. The question is why it took this long.

- Vendor invoice integrity: Reports suggest some vendors used to route the payments may have generated questionable invoices, potentially creating GST input tax credit complications. That’s a second layer of irregularity the normal financial controls should have flagged.

- RBI reporting obligations: Differential deposit rates above a certain threshold require regulatory reporting. The structuring of these payments specifically to avoid that reporting channel suggests a deliberate bypass of regulatory disclosure.

What This Means for Investors and Markets

HDFC Bank is not a small-cap with weak oversight — it’s India’s largest private lender, with a market cap that places it among the most valuable companies in the country. Governance concerns at this level don’t stay contained to the boardroom.

The Immediate Market Impact

- Stock price signal: Two significant single-day drops — 9% in March after the chairman’s exit, and ~2.5% in late May after the investigation published — reflect the market pricing in governance risk, not just financial risk. That’s different, and typically stickier.

- Foreign institutional investor sensitivity: FIIs holding HDFC Bank positions are acutely sensitive to governance signals. A chairman resigning over ethics at India’s largest private bank is the kind of red flag that shows up on ESG scorecards globally.

- Deposit confidence: This is perhaps the most important long-term consideration. If the story gets legs — particularly the angle around differential rates being offered to government agencies — retail and institutional depositors may start asking questions about what arrangements exist elsewhere.

The Deeper Structural Question

HDFC Bank has been in a transitional phase since the landmark merger with HDFC Ltd in July 2023. It’s a $40 billion integration exercise that doubled the balance sheet and brought enormous complexity into the organisation. Integration periods are precisely when governance frameworks get stretched — teams are reorganised, oversight structures are in flux, and the pressure to maintain deposit growth is intense.

That context doesn’t excuse what allegedly happened. But it does explain the conditions under which it could happen. And it raises a genuine question for investors: in a bank this large, undergoing this much structural change, is the governance architecture keeping pace?

What Should Happen Now

Corporate governance failures don’t fix themselves by acknowledging they happened. What matters is the response — and right now, HDFC Bank’s public posture has been notably cautious.

- Independent external review: The internal probe and the legal firm review serve different purposes. An independent board-commissioned external governance audit — with results shared with shareholders — would do more to restore confidence than any denial.

- RBI cooperation and disclosure: Proactive engagement with the regulator, rather than waiting for a direction, signals that the institution is taking the violation seriously and not managing a PR problem.

- Action on named officials: The probe reportedly named over ten senior officials as bearing responsibility. What happens next — accountability, reassignment, or silence — will define whether this is treated as a genuine governance failure or a compliance footnote.

- CEO and CFO statement to shareholders: Given both were reportedly present at discussions where the arrangement was devised, a clear public accounting — separate from routine quarterly commentary — is arguably owed to the bank’s shareholders and depositors.

- Systemic review of institutional deposit deals: Not just MSRDC — any institutional arrangement where off-balance-sheet compensation may have been used to bridge rate differentials deserves audit scrutiny now.

Final Read:

₹45 Crore Is Not the Point.

The story is what the arrangement reveals: that somewhere in the decision chain at one of India’s most respected financial institutions, people concluded that disguising interest payments as marketing spend was an acceptable way to win a government deposit. And that no one — until a routine audit happened to look — thought to stop it.

Corporate governance isn’t about preventing fraud. It’s about building systems where the instinct to do something questionable is met with a structure that makes it difficult, visible, and costly. By that standard, something failed here — regardless of what the external legal review eventually concludes.

For investors, the question now is whether HDFC Bank’s response is commensurate with what the probe found — or whether the institution is managing a reputational timeline rather than genuinely reckoning with a governance one. The difference between those two responses will determine whether this becomes a footnote or a turning point.

Banking Analysis — May 2026