🇮🇳 India Economy | 2025–26

The “3F”

Warning:

India’s

Fuel Crisis.

Every few months, something happens in the Indian economy that looks like a statistic on the surface — but hits your daily life in very real ways. This is one of those moments.

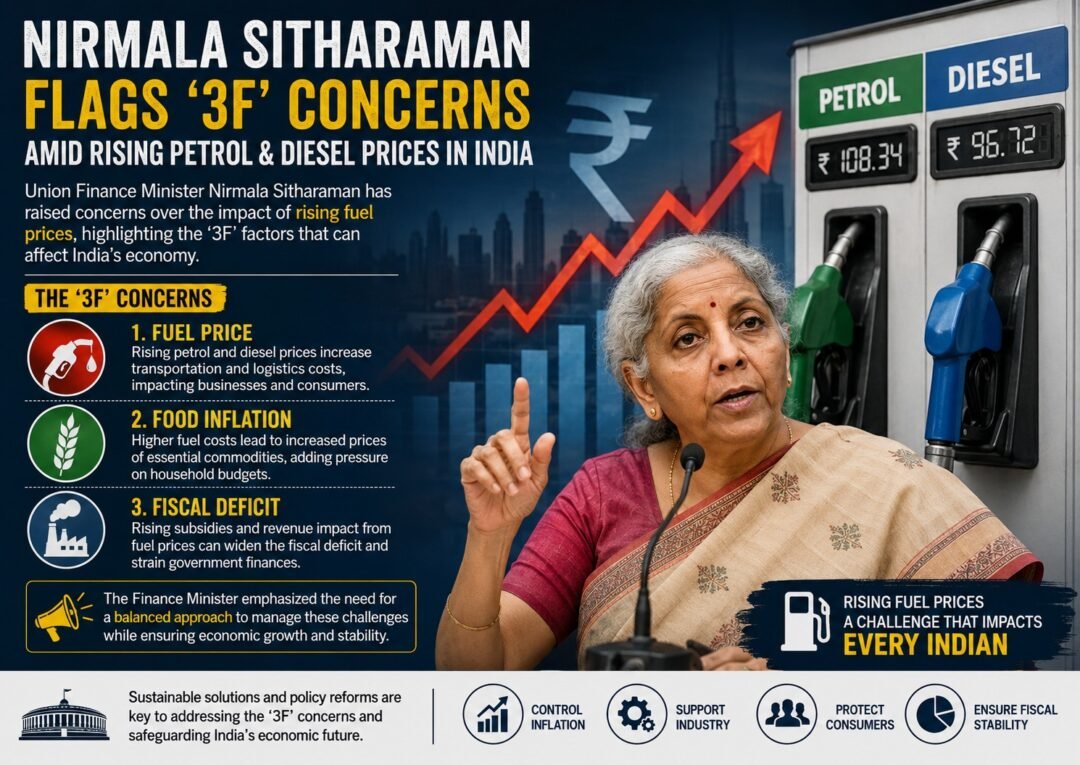

Finance Minister Nirmala Sitharaman has flagged what she calls the “3F” problem — Food, Fuel, and Fertiliser — as the three biggest pressure points threatening India’s economic stability. And when petrol and diesel prices start climbing again, those three words stop being budget jargon and start being the reason your grocery bill and your commute cost more this month than last.

This piece breaks down exactly what the 3F warning means, why fuel is at the centre of it, and what it actually signals for India’s middle class, professionals, and anyone trying to plan their finances in a volatile macro environment.

What Is the “3F” Warning — And Why Now?

It’s not a new phrase. The “3F” framework — Food, Fuel, Fertiliser — has been used in international economic circles for years to describe the trio of commodities that, when stressed simultaneously, can push inflation to dangerous levels. Especially in import-dependent economies.

But when India’s Finance Minister uses it in the current context, it carries a specific weight. Because right now, all three are under pressure at the same time. Global crude oil prices have been elevated. Fertiliser costs — which are closely tied to energy inputs — have remained high since the Russia-Ukraine conflict disrupted global supply chains. And food inflation, which never really cooled fully after COVID, is still stubborn.

The timing of Sitharaman’s warning isn’t accidental. With West Asia tensions continuing to drive crude oil volatility in 2025–26, India finds itself in the classic difficult position — heavily dependent on imported oil, unable to fully absorb the global price shock, and trying to balance retail fuel prices against fiscal prudence and voter sentiment.

Where Petrol & Diesel Prices Actually Stand Right Now

Let’s get specific. Because the “prices are high” conversation is useless without numbers.

In Delhi, petrol is hovering around ₹94.77 per litre and diesel around ₹87.67 per litre as of mid-2025. In Mumbai, those numbers are higher — petrol crosses ₹104 because of local taxes. Across smaller cities and semi-urban India, the variance is wide, but the direction is the same: upward pressure.

What’s important here isn’t just the per-litre number. It’s the context. Retail fuel prices in India were last revised downward in mid-2024 as an election-season measure. Since then, international crude has crept back up, and the spread between what oil marketing companies (OMCs) are actually paying for crude and what they’re charging at the pump has been quietly getting tighter — or in some cases, reversing.

🔑 Why Fuel Prices in India Are Complicated

- Dynamic Pricing on Paper, Political Reality in Practice: India technically has a “dynamic” fuel pricing system where OMCs revise prices based on international crude. In practice, revisions are often delayed — especially near elections — creating a gap that OMCs absorb as under-recoveries, which then shows up as pressure on PSU balance sheets.

- State Taxes Are a Huge Variable: Central excise duty plus state VAT can together account for nearly 50–55% of the retail price of petrol in some states. That’s why Mumbai’s price and Delhi’s price can differ by ₹10+ even when crude is the same.

- OMC Health Matters for Your Portfolio: IOCL, BPCL, and HPCL — the three major public sector oil retailers — swing between profits and losses based on this gap. When crude is high and retail prices are held, their margins get crushed. Their stock performance, dividends, and capital expenditure plans all get affected.

- Inflation Pass-Through Is Not Immediate: There’s typically a 4–8 week lag before a diesel price hike shows up as higher vegetable prices in your local market. But it always shows up. Truck operators, cold chain logistics, last-mile delivery — all of it runs on diesel.

What This Means for India’s Middle Class

This is where the macro conversation gets personal. And it’s where most financial media drops the ball — they explain the geopolitics and the policy, but they don’t connect it to the actual lived experience of a salaried professional in Gurugram or a business owner in Pune.

So let’s be honest about it.

Your Monthly Budget Is Getting Squeezed From Both Ends

Higher fuel prices don’t just mean you pay more at the pump. Your grocery delivery costs more because the last-mile logistics cost more. Your office commute — whether it’s fuel for your own vehicle or the CNG price hike that auto and cab drivers pass on to you — gets more expensive. The vegetables you buy are priced higher because the farmer’s input costs (fuel + fertiliser) went up. The packaged goods on your supermarket shelf have a fuel surcharge quietly baked into their prices.

Meanwhile, your salary hasn’t gone up by the same amount. That compression — flat income against rising costs — is the defining financial reality for a large section of India’s urban middle class in 2025.

“It’s not one big bill. It’s fifty small ones that quietly drain your savings every month.”

The Middle Class 3F Reality — 2025

The EMI Connection You’re Not Thinking About

Here’s the link that most people miss. When fuel prices stay elevated, inflation stays sticky. When inflation stays sticky, the RBI has less room to cut interest rates. When rates stay higher for longer, your home loan EMI stays higher for longer. Your car loan doesn’t get cheaper. The business loan you were waiting to take at lower rates gets delayed.

The 3F warning isn’t just about OMC margins or government fiscal math. It’s directly connected to the interest rate environment — which is directly connected to how much you pay every month for your mortgage.

The Fuel Price Timeline — How We Got Here

What Professionals & Investors Should Actually Do

Generic “be careful with spending” advice is useless here. Let’s talk about what the 3F environment actually means for specific financial decisions — the ones a salaried professional, a small business owner, or a retail investor might actually make in the next 6–12 months.

For Your Personal Budget

- Audit your fuel exposure, not just your fuel bill: The direct pump cost is one thing. But look at how much of your monthly grocery, food delivery, and logistics spend is fuel-indexed. That’s where the real squeeze is happening — and where small behaviour changes (consolidating trips, switching to CNG or EV) actually have compounding impact over time.

- Don’t assume EMI relief anytime soon: If you’re expecting the RBI to cut rates significantly in the next two quarters and you’re making financial plans based on that, recalibrate. Sticky inflation — driven partly by fuel costs — is pushing that timeline further out than the consensus expected 12 months ago.

- Food costs will stay elevated: The fertiliser-food link means agriculture input costs are still high. The diesel-logistics link means last-mile food costs are still elevated. Budget for food spending to remain 15–20% higher than your pre-2022 baseline well into 2026.

For Equity Investors

- Indian OMCs are a nuanced play — not a simple one: IOCL, BPCL, and HPCL trade at attractive valuations when global crude is high AND when the government allows retail price passthrough. When crude is high but prices are held politically, they become value traps. The signal to watch is the government’s willingness to revise retail prices — that’s the unlock event, not just the crude price itself.

- Avoid FMCG companies with high logistics sensitivity on the input side: Companies that ship heavy, bulky products with thin margins — packaged foods, building materials — face margin pressure in a high-diesel environment. Consumer staples with pricing power are safer; high-volume logistics-dependent businesses are exposed.

- Indian defence and energy transition stocks are structural: The 3F crisis is accelerating India’s push toward energy self-sufficiency. Solar, green hydrogen, domestic refining capacity, EV infrastructure — these aren’t speculative themes anymore. They’re policy priorities backed by real budget allocation. The investment thesis has multi-year legs.

- Renewables and EV as a hedge on fuel dependency: Every percentage point that India reduces its crude import dependence structurally reduces the 3F vulnerability. Companies involved in that transition — Adani Green, NTPC Renewables, Tata Motors EV division — are effectively hedges on this exact problem.

For Small Business Owners

- Build fuel cost escalation into contracts now: If you’re entering into fixed-price service or supply contracts that run 12+ months, explicitly include a fuel price escalation clause. The days of assuming stable logistics costs are over for the foreseeable future.

- Review your working capital cycle: Higher input costs — especially in manufacturing, food processing, or any logistics-heavy business — mean you need more working capital to fund the same level of operations. If your working capital credit line hasn’t been reviewed recently, now is the time.

Final Read:

Three Letters. Real Consequences.

For India’s middle class, that means navigating an environment where costs are stubbornly high, rate relief is delayed, and the government is walking a very fine line between fiscal discipline and retail price control. There’s no clean answer. But there is a clear-eyed way to prepare — and that starts with understanding the mechanism, not just complaining about the outcome.

Food. Fuel. Fertiliser. Three words that don’t sound alarming on their own. But together, in the current global environment, they’re the most important variables in India’s economic story for the next 12–18 months.

India Economy — 2025–26