🏦 Banking & Fiscal Policy | May 2026

RBI Cuts Its

Safety Net.

Sends ₹92,000 Cr

to Delhi.

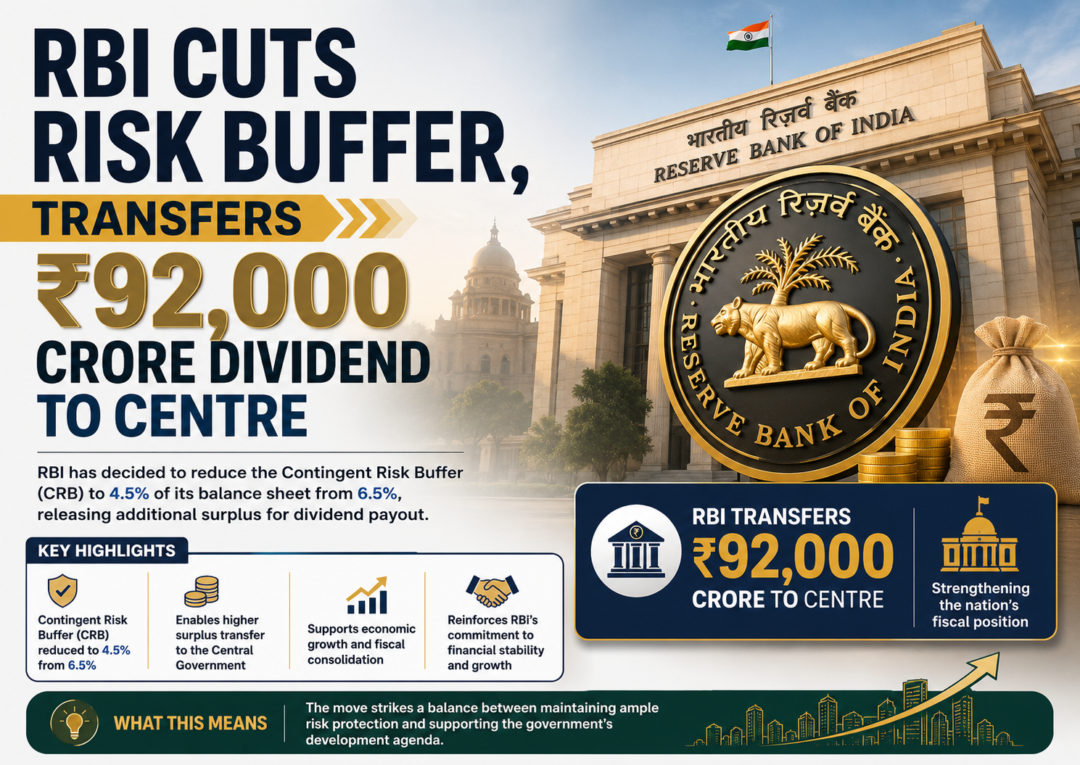

Somewhere between a routine board meeting and a headline that flew past most people’s feeds, India’s central bank did something significant. The Reserve Bank of India quietly reduced its own financial cushion — its internal risk buffer — and handed over ₹92,000 crore to the central government as dividend.

That number sounds big because it is. But here’s the thing — it’s also sharply lower than last year’s ₹2.11 lakh crore transfer. So is this a story about the government getting less money? Or about the RBI tightening its own belt at a delicate time? Or both?

The answer is: both. And understanding why this matters — not just for the government’s balance sheet, but for interest rates, banking liquidity, and the broader economy — is exactly what this piece is about.

First — What Is the Contingency Fund?

Most people know the RBI as the body that sets interest rates and prints currency. But there’s another side to it — the RBI is also a massive financial institution with its own balance sheet, income, and reserves.

One of those reserves is called the Contingency Fund (CF). Think of it as the RBI’s own emergency savings — money set aside to absorb unexpected shocks. Currency crises. Sudden depreciation in its foreign exchange holdings. A global financial event that forces it to intervene. The CF is the buffer that lets the RBI act without needing a government bailout.

So when the RBI now sets the CF at 6% — right at the lower end of the recommended band — and then transfers ₹92,000 crore, it’s saying: “We’re comfortable at this level of buffer, and everything above that goes to you.”

Whether 6% is enough in today’s environment is the real debate. And it’s a sharper one than most people are having.

Why ₹92,000 Crore and Not More?

Last year, FY25, the RBI transferred a record ₹2.11 lakh crore to the government. That was extraordinary — driven by bumper income from foreign exchange operations, higher returns on bond holdings, and significant valuation gains on its dollar reserves as the rupee depreciated.

This year is different. The income environment has moderated. The RBI’s operational surplus — its income minus expenses — is lower. And crucially, the board chose to retain more within the CF rather than push out the maximum possible transfer.

Where Does RBI Income Come From?

This is worth understanding because it explains why the dividend fluctuates so much year to year. The RBI earns income from several sources:

- Interest on domestic government securities — the RBI holds a portion of government bonds as part of its monetary operations.

- Returns on foreign currency assets — India’s foreign exchange reserves (over $640 billion) are invested in safe overseas instruments. Interest and capital gains from these flow to the RBI’s income.

- Valuation gains on forex reserves — when the rupee weakens against the dollar, the rupee value of RBI’s dollar holdings rises. This creates accounting income that can be transferred.

- Fee income from banking operations — clearing, settlement, and regulatory functions also generate earnings.

In FY25, all four of these ran hot. In FY26, the combination was less favorable. Foreign exchange valuations were more muted, and global bond yields compressed returns. Result: a smaller surplus, a smaller transfer.

What This Means for Government Finances

Here’s where it gets practically important. The Union Budget for FY26 projected a fiscal deficit of 4.4% of GDP. To hit that target, the government needs its revenue projections to hold — and non-tax revenue, which includes the RBI dividend, is a meaningful part of that math.

The government had likely budgeted for a dividend in the range of ₹1–1.2 lakh crore, based on the FY25 precedent and general optimism. Getting ₹92,000 crore instead creates a gap. Not a catastrophic one, but a real one.

🔑 How the Government Plugs the Gap — Options on the Table

- Compress capital expenditure: The easiest lever but the most damaging — cutting capex slows infrastructure build-out, which has been the engine of India’s growth story. The government will resist this unless it has to.

- Push disinvestment harder: Asset sales (PSU stakes, CPSE listings) can generate one-time revenue. But the track record on disinvestment timelines in India is patchy — markets have to cooperate, deals have to close.

- Rely on stronger-than-expected tax collections: GST collections have been running strong in FY26. If that continues, it can partially offset the dividend shortfall without any spending cuts.

- Accept a slight fiscal slippage: Missing the 4.4% target by 10–20 basis points is not a market-breaking event if accompanied by credible medium-term consolidation messaging. Markets will tolerate a small miss if the narrative holds.

- Defer some spending to Q4: A timing trick — push expenditures into March, keep the headline deficit number for the current fiscal technically contained.

The honest read? The government will probably use a combination of all of the above. But the RBI dividend shortfall makes the FY26 fiscal math tighter than it looked in February.

The Bigger Question — Is 6% Enough of a Buffer?

This is the debate that institutional economists are having quietly, and that the financial press hasn’t quite crystallized yet.

The Bimal Jalan committee set the 5.5%–6.5% range in 2019 — before COVID, before the Russia-Ukraine war, before global inflation ran at 40-year highs, and before the current phase of West Asian geopolitical tension started reshaping energy and currency markets.

The world has changed. The risks that central banks face — sudden capital outflows, currency defense operations, systemic banking stress, commodity shock spillovers — are structurally higher than they were in 2019. Setting the CF at 6% — the lower end of a framework designed for a more stable world — is a choice that deserves scrutiny.

“A central bank’s credibility is partly measured by whether it looks underfunded in a crisis.”

Institutional Risk Management Perspective — 2026

To be clear: the RBI’s balance sheet is still large and the CF in absolute rupee terms is substantial. India’s forex reserves provide an additional buffer. This is not an alarm call. But the directional choice — trim the buffer, transfer more — is worth watching as a trend, not just a one-year decision.

The Context Behind This Decision

What Professionals Should Actually Watch

For banking professionals, fiscal analysts, and market participants — here’s where this decision has real downstream implications.

For Bond Market Participants

- Liquidity infusion effect: When the government receives this ₹92,000 crore, it spends it — on salaries, subsidies, capex, scheme disbursements. That money flows back into the banking system, improving systemic liquidity. Bond markets tend to respond positively to RBI dividend transfers because of this liquidity channel.

- Government borrowing programme: If non-tax revenue falls short of budget, and the government doesn’t want to cut spending, it borrows more. Watch the revised borrowing calendar closely. Any upward revision in government securities supply puts upward pressure on yields.

- Short-end rates: The liquidity boost from the RBI transfer gives the central bank more room to manage short-term rates. This is actually a modest positive for the rate cut trajectory — more system liquidity means the RBI doesn’t need to pump in money through other channels.

For Banking Sector Analysts

- PSB recapitalization probability: In years when the RBI dividend is lean, the government has less headroom to recapitalize public sector banks through budget allocations. This is worth tracking for PSB credit profiles — though the current cycle of improved PSB profitability reduces the immediate need.

- Credit growth vs. deposit mobilization: Improved system liquidity from dividend transfer can ease tight credit conditions marginally. For banks running tight on deposits (a real issue in FY26), this provides some breathing room.

- Yield curve shape: A slight softening at the short end while long yields remain sticky (due to fiscal uncertainty) would steepen the curve — which is broadly positive for bank net interest margins.

For Macro and Equity Analysts

- Watch the revised fiscal math in July: The Union Budget mid-year review typically surfaces in July–August. If GST collections disappoint or capex execution slows, the dividend shortfall becomes harder to absorb quietly.

- Rupee implications: A smaller RBI surplus partly signals more cautious forex intervention posture. If the RBI is building back its CF rather than running it lean, that’s a signal of institutional conservatism — which typically supports the rupee’s credibility, even if it reduces short-term transfer income.

- Rate cut trajectory: The RBI’s decision to maintain the CF at 6% also sends a subtle signal about its own risk assessment — it sees enough uncertainty ahead to want a full buffer. That’s not an institution telegraphing aggressive rate cuts. Markets pricing in more than 50bps of cuts in FY26 may be slightly ahead of the curve.

Three Scenarios Worth Tracking

- Soft Landing (~50% probability): GST collections stay strong, disinvestment delivers partially, government absorbs the dividend shortfall without meaningful capex cuts. Fiscal deficit prints at 4.5–4.6%, RBI cuts rates 25–50bps in H2 FY26. Bond yields drift lower. Markets broadly stable.

- Fiscal Squeeze (~30% probability): Tax collections disappoint, oil stays high (rupee pressure), government faces hard choices between capex and deficit. Borrowing programme revised upward. Yields firm up, RBI rate cut window narrows. Equity multiples compress on rate uncertainty.

- Windfall Surprise (~20% probability): Forex gains in H2 FY26 give the RBI unexpected income — a scenario where the full-year picture improves. Government receives an interim transfer or the next year’s dividend cycle recovers sharply. Fiscal math eases. This is the bull case that bond market optimists are implicitly holding.

Final Read:

This Isn’t a Crisis. But It Is a Signal.

The government will manage. India’s macro fundamentals — strong domestic demand, improving tax collections, a well-capitalized banking system — provide real resilience. But the easy fiscal arithmetic of FY25, when a record RBI dividend made the numbers work almost effortlessly, is gone. The heavy lifting now falls back on revenue mobilization, expenditure discipline, and execution.

For professionals watching India’s macro story: the RBI dividend is one of those data points that most people file away and move on from. The smarter move is to read it as a diagnostic — of the RBI’s own risk appetite, of the government’s fiscal flexibility, and of the underlying health of the monetary-fiscal relationship that quietly determines so much of how India’s economy actually functions.

The safety net got trimmer. The transfer got smaller. The questions it raises are bigger than either headline suggests.

Banking & Fiscal Analysis — May 2026