🌐 Geopolitical Analysis | May 2026

The Strait That

Chokes Oil —

And Now Helium 2026 .

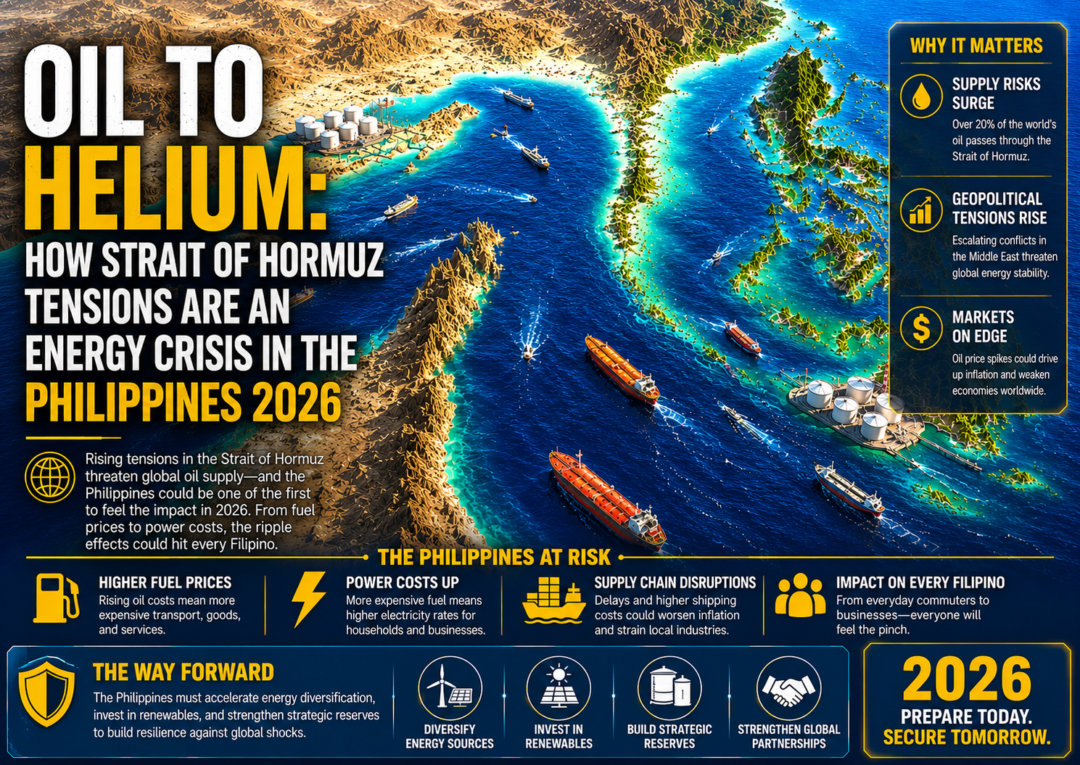

Picture a single lane on a highway that carries a fifth of the world’s oil. Now imagine that lane is located between two countries that are — to put it diplomatically — not on great terms. That’s the Strait of Hormuz in 2026. A narrow 33-kilometre-wide channel separating Iran from Oman, and one of the most consequential pieces of water on the planet.

Most people know the oil story. Fewer know that the same geography is now creating a quiet crisis in an entirely different commodity — helium. And that’s where this story gets genuinely interesting.

The escalating tensions in West Asia haven’t just pushed oil above $90 a barrel. They’ve triggered a cascading set of supply chain disruptions that reach well beyond energy desks and into industries you’d never expect — from semiconductor fabrication to MRI machines to the rockets being launched into orbit.

First, The Oil Picture — And Why It’s Different This Time

The Strait of Hormuz has always been in the background of global energy markets — a threat that’s priced in but rarely acted on. Iran has made noises about closing it before. In 2012. In 2019. Markets flinched, then recovered. Analysts called it posturing. Most of the time, they were right.

But 2026 is different. Not just because the rhetoric is louder — it’s because the underlying conditions have changed. Global oil inventories are thin. Underinvestment in new production over the past several years means there’s less cushion. And critically, the demand side hasn’t collapsed like it did during COVID. Asia is still hungry for energy.

There’s also a geography problem that didn’t exist in quite the same way before. The Houthi operations in the Red Sea — running parallel to Hormuz tensions — have already forced massive shipping reroutes around the Cape of Good Hope. That adds roughly 10–14 days to shipping times from Asia to Europe. Insurance premiums for Gulf corridor tankers have surged. The cost of getting oil from where it’s drilled to where it’s needed has gone up structurally, not just temporarily.

The Chain Reaction No One Is Mapping Fully

Here’s how it actually connects. Oil prices rise → shipping costs rise → consumer inflation climbs → central banks can’t cut rates as planned → borrowing costs stay high → growth slows → equity multiples compress. That chain is already playing out in 2026 data. But the helium thread running parallel to it? That one almost nobody is watching.

Now The Part Nobody’s Talking About: Helium

Helium. You probably associate it with birthday balloons or the occasional funny voice. But the helium that actually matters economically has nothing to do with parties. It cools the superconducting magnets in MRI machines. It’s used in semiconductor chip fabrication. It’s essential for certain rocket propellants and aerospace testing. It keeps fiber optic cables cool during manufacturing.

And here’s the thing — Qatar is the world’s second-largest helium exporter, after the United States. Qatar’s helium — extracted as a byproduct of natural gas processing — exits the Gulf through the same chokepoint that oil does. The Strait of Hormuz.

“It’s not just oil that flows through that strait. It’s the coolant for the machines that build your chips and scan your brain.”

Supply Chain Analyst Perspective — 2026

Any meaningful disruption to Hormuz shipping — even a partial one, even a temporary insurance-driven shutdown of certain tanker routes — hits helium supply in ways that cascade quickly into specific industries. And unlike oil, there’s no strategic reserve for helium. No OPEC equivalent. No stockpile waiting to be released to calm markets.

Why Helium Supply Is Already Fragile Going Into This

The helium market entered 2026 already under stress. The United States — which historically held the world’s largest federal helium reserve — has been in a drawn-out process of privatising and winding down that stockpile since 2013. New production capacity has come online (notably in Russia and Qatar), but it hasn’t kept pace with demand growth from semiconductors and healthcare.

The result is a market that was already running tight, meeting a geopolitical disruption scenario that it’s structurally ill-equipped to absorb. Chipmakers and hospital procurement teams are watching Hormuz in ways they never had to before.

The Industries Most Exposed

The disruption pattern isn’t uniform. Understanding who gets hit first — and hardest — is where the real analytical work lives in 2026.

Chip fabrication uses helium extensively — for cooling, as a carrier gas, and in specific deposition processes. Taiwan, South Korea, and Japan are the major manufacturing hubs, and they’re all entirely import-dependent for helium. Any sustained supply squeeze gets felt fast in fab lead times.

MRI machines run on superconducting magnets cooled by liquid helium. Hospitals maintain buffer stocks, but they’re not infinite. A prolonged disruption — even a few months — would force procurement teams into a very uncomfortable spot. Elective procedures could face delays in supply-constrained scenarios.

Helium is used to pressurise rocket propellant tanks and in testing systems for both commercial and government launch programs. SpaceX, NASA, and various national space agencies all have helium dependencies. Launch schedules have real sensitivity to supply availability.

Meanwhile, integrated oil companies and upstream producers are thriving. Brent above $90 turns marginal Gulf projects into high-margin operations. Companies with locked-in long-term supply contracts are performing strongly. The disruption that hurts one side of the economy is directly enriching this one.

The Cape of Good Hope rerouting isn’t just a time problem — it’s a cost problem. Fuel consumption climbs, crew costs increase, vessel utilisation shifts. Carriers like Maersk and Hapag-Lloyd have flagged these headwinds. For just-in-time supply chains, weeks of extra transit time is a structural problem, not an inconvenience.

India imports roughly 85% of its crude oil and is a significant helium importer for its growing semiconductor and healthcare sectors. Higher oil widens the current account deficit and pressures the rupee. At the same time, India’s diplomatic positioning — maintaining Gulf relationships while deepening Western ties — gives it unusual flexibility in navigating the disruption.

How We Got Here — The Escalation Timeline

What Strategic Thinking Looks Like Right Now

The professional response to a dual-commodity supply disruption like this isn’t panic — it’s structured scenario planning. Here’s what that actually looks like in practice.

🔑 Professional Frameworks for Hormuz Risk — 2026

- Map your indirect exposures first: Most portfolio managers know their direct energy exposure. Far fewer have mapped their indirect helium exposure — through semiconductor holdings, healthcare equipment companies, or aerospace positions. This is a gap that 2026 is forcing people to close fast.

- Helium alternatives are real but slow: There are alternative helium sources — US private production, new Australian fields, some Russian supply — but they can’t scale overnight. In a disruption scenario, the market tightens before it adjusts. That lag is where the pain concentrates.

- Dual disruption pricing: Markets are currently pricing oil disruption risk reasonably well. They are not fully pricing the downstream helium-semiconductor-healthcare chain. That gap — between what’s being priced and what the actual risk is — is where informed analysis lives.

- Energy sector tilt vs. tech sector drag: The same geopolitical event that’s pushing energy stocks higher is creating a headwind for semiconductor valuations — both through direct helium supply uncertainty and through the oil-inflation-rates-multiples chain. Being long energy and long semiconductors simultaneously requires careful position sizing right now.

- India-specific calculus: Indian semiconductor ambitions under PLI schemes, combined with India’s oil import dependence and its Gulf diplomatic positioning, create a genuinely unique exposure profile. The trade-off between rupee pressure from oil and geopolitical access to Qatari helium supply isn’t something generic EM models capture cleanly.

- De-escalation asymmetry: A diplomatic breakthrough — ceasefire, backchannel deal, meaningful Houthi disengagement — would trigger sharp oil price correction, immediate helium risk premium compression, and a relief rally in semiconductor stocks. The professional move includes being positioned for that scenario, not just the escalation playbook.

Three Scenarios Worth Modelling

- Contained Tension (~50% probability): Hormuz remains open but with elevated risk premium. Oil holds $85–100. Helium market stays tight but functional. Semiconductor supply chains adapt with buffer stocking and partial alternative sourcing. Markets grind with elevated volatility. Energy and defence outperform; semiconductors face valuation pressure but not supply crisis.

- Diplomatic Progress (~25% probability): Backchannel agreements reduce Houthi activity, Iran-Israel tension de-escalates meaningfully. Oil falls to $70s. Hormuz risk premium compresses across oil and helium. Semiconductor stocks rally as supply anxiety eases. Central banks regain rate cut optionality. Classic relief rally setup — but fast-moving and easy to miss.

- Escalation / Partial Hormuz Disruption (~25% probability): Any meaningful interference with Hormuz shipping — even temporary. Oil spikes toward $120+. Helium spot prices surge as Qatar exports face uncertainty. Semiconductor supply chains face genuine input shortages within 2–3 months. Healthcare helium buffers begin depleting. Equity markets correct 15–25%. Stagflation risk repriced sharply. This is the tail to hedge, not predict.

The Strait Connects

More Than You Think.

The tensions in West Asia didn’t create these vulnerabilities — they exposed them. Supply chains that had been optimised for efficiency over resilience are now facing the cost of that trade-off. And markets that priced in only the oil dimension of Hormuz risk are waking up to a more complex picture.

What makes 2026 genuinely different from previous West Asia tension cycles isn’t just the magnitude of escalation — it’s the breadth of what’s connected to that single narrow channel. Oil. Helium. Chips. Hospitals. Rockets. They all have a thread running through 33 kilometres of contested water.

The professionals navigating this well aren’t the ones who predicted the escalation. They’re the ones who mapped the full network of dependencies before the crisis hit — and positioned for optionality across outcomes rather than certainty in one direction. That approach doesn’t make headlines. But in six months, it makes returns.

Geopolitical Analysis — May 2026